Highly concentrated markets delay economic participation

A pointed reminder to society of why the wheels of economic participation must turn faster is found in the words of former President Nelson Mandela: "A nation is transformed when its people choose responsibility and excellence as acts of freedom".

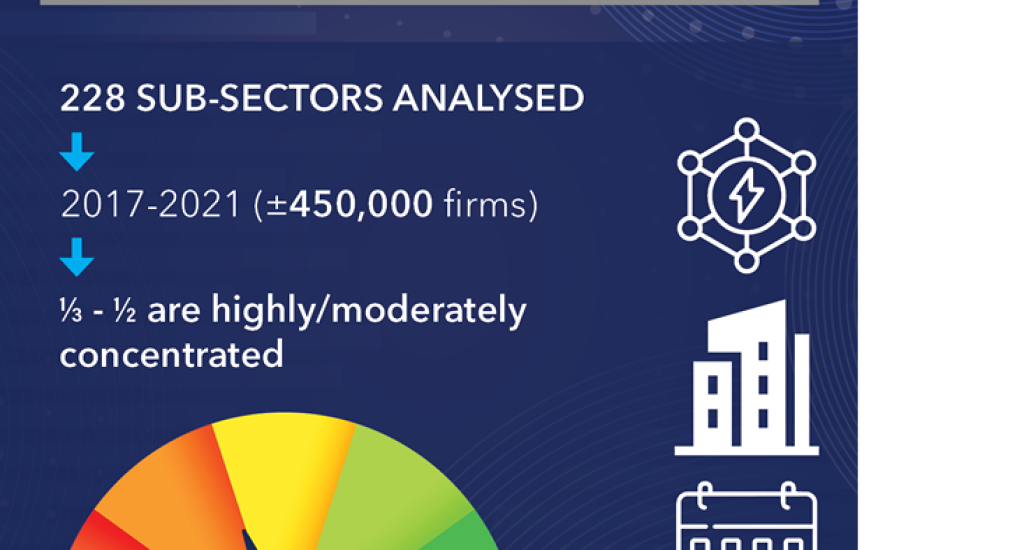

When markets are tight, the economy feels tight. The Competition Commission’s second Concentration Report is indicative of steps in the right direction, but it delivers a blunt message: in too many parts of the economy, economic contenders still struggle to enter, survive and scale.

If we want faster growth and more jobs, competition has to be practical, not rhetorical.

Understanding market concentration

Think of the last time a price hike rippled through your business. Fuel hikes, freight follows, packaging rises, and everyone down the chain gets squeezed. That squeeze is not only about inflation. It is also about who has the power to set terms in the middle of the economy.

That power is what economists refer to as “concentration”. In plain terms, it is a market where a few firms can raise prices, restrict access, or decide which suppliers get a chance. The World Bank and the International Monitory Fund have warned that high concentration drags on growth and jobs, a concern echoed in government’s Medium Term Development Plan. Closed markets make for a smaller economy.

The report gives an economy-wide view of where power sits and where it is shifting. There is real movement. The share of highly concentrated markets fell by about five percentage points, and most sectors that were highly or moderately concentrated became less so. It is not a victory lap. It is proof that markets can open.

The hard part is where concentration is most stubborn: the “pipes and platforms” of the economy. Energy inputs, transport corridors and communications networks still show durable concentration, often with half to two-thirds of sub-sectors sitting in the highly or moderately concentrated range. These are the cost base of everything else.

When access to fuel, freight, ports, data or spectrum is controlled by a few, every downstream business pays, and every entrant starts metres behind.

Dominance vs competition

A market with a few big players can still be competitive if they genuinely fight for customers. The bigger risk is a single dominant firm that can choke rivals through exclusive contracts, control of infrastructure, data, or standards. The tougher question is this: can a challenger realistically grow?

The report’s most uncomfortable finding is participation. South Africa has many micro businesses, but too few firms that graduate into stable, job-creating mid-sized companies. Micro, Small and Medium Enterprises (MSMEs) account for only about 22% of economic turnover here, compared with more than 50% in many Organisation for Economic Cooperation and Development economies. Medium-sized companies make up only around 4% of firms.

Scaling blockages for MSMEs

Scaling is where the blockage shows. The top 10% of firms account for about 91% of economic activity, while the bottom 50% account for roughly 1%. The Covid- 19 then hit smaller firms hardest: 22% of MSMEs shrank, and exit rates rose to 12% from an average of 8% before the pandemic. Yet MSMEs are twice as employment-intensive as large firms, accounting for about 44% of jobs while representing only 22% of turnover.

So what now? The report points to three places where action can unlock competition quickly: enforcement that clears unfair obstacles, regulation that stops blocking entry, and technology that widens choice.

Start with enforcement. Competition law is not anti-business. It stops dominant firms from using their weight to keep rivals out. Abuse of dominance cases, market inquiries and advocacy can open routes to market. Merger control matters too, because it is easier to prevent harmful consolidation than unwind it later.

Then regulation. Some rules protect the public interest. Others, through licensing delays, complex permits or poor implementation, become a moat for the incumbents. That is why the Commission’s Regulatory Review Project, published in April 2026, is inviting businesses to identify rules that are overly restrictive or badly implemented, and to propose fixes.

The aim is pro-competition regulation that protects people without quietly shutting the door on new entrants. This would help reduce the unnecessary red tape.

Technology can also shift power fast by changing the gatekeeper. Streaming, fintech, eCommerce and renewables have all widened options. But disruption is not automatically inclusive, and new markets can recreate old concentration. The policy task is to back innovation while keeping markets contestable.

The priority now is scale. South Africa needs more medium-sized and larger challenger firms that can compete, invest and hire.

That means removing the bottlenecks that stop promising firms from growing, such as access to finance, logistics, data, key inputs and procurement opportunities. It also means targeting conduct that keeps markets closed, not only conduct that nudges prices up.

Avoiding monopoly in reform

One more caution: restructuring state-owned enterprises should not replace a public monopoly with a private one. Where reform is on the table, opening markets and separating monopoly functions first can create real space for entry and investment. Structure determines whether competition is even possible.

The second Concentration Report is not a set of tables to admire. It is a challenge to act. Deconcentration is pro-investment, pro-innovation and pro-jobs. The practical test is simple: can a capable firm enter, expand and win customers without being blocked by gatekeepers or paper barriers? If the answer becomes yes, South Africa’s next wave of firms can do what the economy needs most: compete, innovate and hire.

videos & photos